Originally published in Spanish in La Izquierda Diario

The debate about the place of robotics, artificial intelligence, genetics and other cutting edge technologies and their role in the capitalist economy gives rise to two clearly antagonistic positions within official economic theory.

On the one hand, there are those who point out that new technologies are on the verge of a giant transformation in productivity generated by a new industrial revolution that will then give birth to a period of economic boom. Promoters of this thesis such as the specialists Erik Brynjolfsson and Andrew MacAfee, authors of The Second Machine Age, argue (as Michel Husson has summarized) that these new technologies bring with them both “good and bad”.

The good is that consumers will benefit through reduced prices. The bad is that there will be a considerable loss of employment in the course of the coming decades as human labor is increasingly replaced by robots. According to the authors, and as quoted by Michael Roberts, “We’re moving to a world where there will be vastly more wealth and vastly less work”. In accordance with this thesis, studies also referred to by Roberts, predict a loss of 7.1 million jobs. These jobs will not be lost in a period of crisis but in one of economic boom, that is – in the 15 major economies of the world over the next five years only two million new jobs will be created.

On the other hand, there are those who can be grouped together under the heading of “skeptics” of a prosperous future arising from the competition between technology and economic growth. Authors such as Robert Gordon – a very important American specialist in productivity – turn this causality upside down. In his recently published book, The Rise and Fall of American Growth , which focuses on economic trends in the United States, Gordon argues against the “techno-optimists”.

While guarding a certain amount of pessimism regarding the potential of existing inventions, Gordon’s rejection of the idea of a spectacular take-off in future productivity is essentially based on two factors: first, the weakness in productivity growth over the previous decade, and second, what he calls the “headwinds” that affect the economy. The combination of these two factors are what leads him to foresee, in contrast to the techno-optimists, much weaker future economic growth than that of the past. It is worth noting that far from the perspective of the “end of labor”, Gordon identifies a shortage of labor power due to low population growth as one of the explanatory “headwinds” of current economic fragility.

For the purposes of analysis, it is necessary to divide this problem of labor productivity into these two parts, although they are without doubt one and the same issue. For reasons of space, we will start with the first problem and then address both in a later installment.

The sense of the Solow paradox

Although there is a generalized idea of the deployment of a great technological advance in recent decades, it is necessary to make a distinction. No one can dispute the development of factors that have revolutionized much of life on Earth, such as information technology, cellular telephones and other things that promise new transformations such as 3D printers, robotics and genetics. But despite all of this, we need to ask ourselves, to what extent do these elements have the ability to modify production output and capacity as a whole or, in other words, labor productivity?

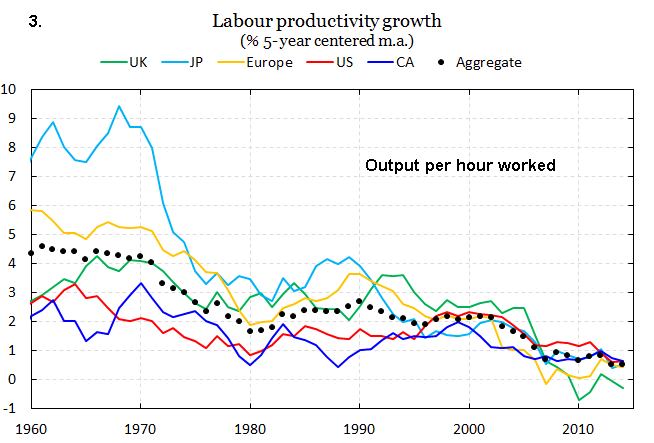

Although productivity has of course increased over the last decades, its growth has been moving at a decreasing rate since the 1970s, as a multiplicity of sources can confirm. In accordance with the data provided by Gordon, while the rate of increase in output per hour rose in the United States at a rate of 2.82% per year between 1920 and 1970, it grew at a lower rate of 1.62% between the years 1970 and 2014. Taking into account the questionable but very much en vogue concept in economic theory of total factor productivity (TFP) that measures the speed in which production grows in relation to the increase of labour and supplies of capital inputs, TFP in the United States grew after 1970 at barely a third of the rate it did between 1920 and 1970. On the other hand, Gavyn Davies shows that the aggregate productivity of the G7 countries shows a downward trend, with a growth rate contracting from 2.5% during the 1970s (compared to a value close to 4% during the 1960s) to just under 1% for the decade of the 2000s.

It is precisely this contradiction between the significant presence of innovative technological means and their weak impact on productivity that gave rise in around 1995 to the paradox that bears the name of Robert Solow, who once quipped, “You can see the computer age everywhere but in the productivity statistics”. However, it is true that shortly after this, statistics did begin to reflect the communion between personal computers and communications in the form of the internet, web browsing and email. As Gordon points out, between 1996 and 2004 the average rate of productivity growth doubled between 1972 and 1996. However, he says, the effect fell apart in 2004 when productivity growth returned to the average rates of 1972-96 despite the proliferation of flat screens, laptops and smartphones in the decade after 2004. With that the Solow paradox then returned to center stage. Michel Husson suggests that the so-called “new economy” which resulted in the revival of productivity in those years was no more than a “high-tech” cycle. Robert Gordon emphasizes by way of contrast that, unlike these few years, the stimulus that electricity generation gave to industrial efficiency led to an increase in productivity that rose strongly at the end of the 1930s and into the 1940s, giving rise to the remarkable average growth rate that extended into the prolonged period that developed between 1920 and 1970.

On the other hand, and returning to the present, the growth rate of productivity in the United States returned after around 2005 to the weak standards of the period, but then suffered a significantly more pronounced deceleration in the years that followed the 2008 crisis. According to data from The Conference Board, U.S. productivity declined from 1.2% in 2013 to 0.7% in 2014, while the estimate for 2015 is a lean 0.6%. Meanwhile, as we previously noted in La Izquierda Diario , the average growth of labour productivity in the developed economies has slowed from 0.8% in 2013 to 0.6% in 2014.

Finally, we need to take into account the accelerated productivity growth in China and the so-called “emerging” countries, which has for years contributed significantly to the increase of the global average. The productivity growth rate of the Asian giant during the 2000s hit an average of 10.7% . However the limits of the “export model” and the subsequent decrease in growth rates have in the last few years imposed a retraction in the increase of the productivity. The rate of productivity growth in the “emerging” economies slowed from 3.4% in 2014 to 2.9% in 2015. According to The Conference Board, the main explanatory factor of this phenomenon is the slowdown in Chinese productivity growth, but the impact of negative productivity growth in Russia and Brazil must also be accounted for.

Erik Brynjolfsson and Andrew MacAfee question whether these statistics can accurately reflect reality. In an extensive Foreign Affairs article referred to by Michael Roberts, Martin Wolf points out that the techno-optimists “respond that the GDP statistics omit the enormous unmeasured value provided by the free entertainment and information available on the Internet. They emphasize the plethora of cheap or free services (Skype, Wikipedia), the scale of (…) entertainment (Facebook), and the failure to account fully for all the new products and services. (…) Moreover, say the techno-optimists, the “consumer surplus” in digital products and services – the difference between the price and the value to consumers – is huge.” Wolf, who relies largely on the concepts of Gordon – responds by saying that on the one hand they need to consider that “the pace of economic and social transformation has slowed in recent decades, not accelerated”. And on the other, with regards to the points raised by the techno-optimists: “These points are correct. But they are nothing new: all of this has repeatedly been true since the nineteenth century. Indeed, past innovations generated vastly greater unmeasured value than the relatively trivial innovations of today”. Among many other aspects Wolf points out that it is necessary to “consider the shift from a world without telephones to one with them, or from a world of oil lamps to one with electric light (…) Over the past two centuries, historic breakthroughs have been responsible for generating huge unmeasured value. The motor vehicle eliminated vast quantities of manure from urban streets. The refrigerator prevented food from becoming contaminated. Clean running water and vaccines delivered drastic declines in child mortality rates. (…) The introduction of the railroad, the steam ship, the motor car, and the airplane annihilated distance.” Without ignoring the importance of today’s developments, Wolf stresses that while many changes have been introduced, the impact of these new technologies on productivity has been modest, “more recent general purpose technologies – biotechnology and nanotechnology, most notably – have so far made little impact, either economically or more widely.”

To tell the truth, the techno-optimists do no more than explain a paradox by appealing to this same paradox. As Michel Husson also points out there are those such as Lawrence Mishel who simply paraphrase Solow: “Robots are everywhere in the news but they do not seem to leave a footprint in the data”.

The dilemma of the techno-optimists

The explanation for the problem of falling productivity growth is not simple and neither are there positions which can be considered to be conclusive. The discussion that is currently underway is a sharp one. In La Izquierda Diario and elsewhere, we have summarized some of today’s the major debates in official economic theory and have proposed some interpretive elements. Various Marxist authors such as the aforementioned Michael Roberts and Michel Husson, on their part, suggest various elements for the construction of an explanatory hypothesis of the matter.

The weakness of investment tends to operate as a common argumentative factor against weak productivity growth. As mentioned in “Secular Stagnation, Foundations and Dynamics of the Crisis” , the question of investment represents a long-standing problem which was partially resolved during the 1990s and the 2000s, but acquired particular intensity after 2008. This question has only intensified with the recent slowdown in China and the “emerging” economies. In order to avoid overwhelming this article with data, we refer the reader to the article cited above.

Michael Roberts has demonstrated an interesting correlation between investment and productivity. He warns that the only phase in which economic efficiency dramatically increased in the United States during the 34 years of the Internet revolution and information and communications technology (ICT) occurred after a surprising jump in capital investment in this area. Productivity began to take off from 1997, which was three years after the start of the strong rise in investment that began in 1994 and corresponded primarily to the ICT sector. Roberts suggests that from that moment, a relationship occurs where for every percentage point of increased investment in GDP, productivity rose by 0.86 points and by 0.89 points 4 years later. Productivity per hour reached a growth rate of 3.6% in 2003, the highest value in half a century. It is precisely this decline in investment – which recovered after a strong downturn in 2001 – that begins in 2005. Not coincidentally, this is the same moment in which (as noted above) productivity returns to the low parameters of the period.

From our point of view, the issue raised by Roberts is of great interest for the contemplation of the question in the title of this article. Do we find ourselves at the gates of a revolution in productivity? Moving the relationship of a few years ago to the present was answered – at least partially – in the 1990s by the Solow paradox. If we were facing a cycle of strong investment and low productivity growth as we were then, perhaps a similar prediction could be made. However, if we consider that the great dilemma in recent years is concentrated in declining investment, something that supporters of the thesis of secular stagnation – and a broad spectrum that includes the IMF – have defined as a growing “savings glut”, it seems highly unlikely that we are standing at the gates of a productivity boom. This is said without any judgment of the value of the quality of new technical developments. The Solow paradox seems to be expressing an even deeper problem than that of the 1990s. Otherwise we would have to ask the techno-optimists: are the statistics that reflect on capital investment also wrong?

Naturally this discussion takes us once again to the complex relationship between the real economy and economic bubbles that we have already dealt with in La Izquierda Diario . But we will speak of this of this in a future article.

Translation: Sean Robertson

{kind=link}